Weekly Brief: Credit

Credit’s $50 Billion Blow for Banks

By Lisa Lee, Gowri Gurumurthy, Davide Scigliuzzo and Olivia Raimonde

Banks are finding it’s only getting harder to offload the roughly $50 billion of debt they committed to provide for leveraged buyouts just a few months ago, and the pain is ramping up as the lenders prepare to post quarterly results.

Wall Street firms are preparing to fund the debt for the LBO of Nielsen Holdings themselves, and potentially for Tenneco as well, as jumping yields and fears of economic trouble ahead are making investors reluctant to buy risky bonds and loans.

Adding to the pressure, Elon Musk has proposed to proceed with his acquisition of Twitter for the original offer price, for which banks led by Morgan Stanley are on the hook to provide around $13 billion of debt financing. That’s part of a $51 billion pipeline of risky committed financings that banks need to sell to asset managers, according to Deutsche Bank estimates.

Providing debt funding for these transactions could pressure banks’ earnings, after they’ve already recorded billions of dollars of writedowns on leveraged loans, junk bonds, and other credit holdings this year. This financing will probably increase their capital requirements under global rules, and constrain their ability to fund new LBOs. The major US banks, including Citigroup and JPMorgan Chase, begin posting third-quarter results next week, with European banks starting later in the month.

For the Nielsen buyout, lenders including Bank of America and Barclays have until around Oct. 11 to offload bonds and loans or else finance the purchase’s $8.35 billion of debt themselves. That’s when a group led by private equity arms of Elliott Investment Management and Brookfield Asset Management is scheduled to close on the LBO.

The banks expect to fund the purchase and hold the debt on their books, according to people familiar. Separately, banks including Citigroup and Bank of America think there’s a high chance they’ll also have to fund the more than $5 billion of debt for Apollo Global Management’s buyout of Tenneco, an auto parts company, the people said. But the situation there is less urgent, because the deal is still in the process of getting regulatory approval before it closes.

Selling this kind of debt is getting harder as investors become more concerned about central banks’ monetary tightening triggering a recession. Bank of America strategists wrote last week that a measure of credit stress had jumped to a “borderline critical zone” in a note entitled, “This Is How It Breaks.”

Last week, a group of underwriters led by Bank of America and Barclays pulled a $3.9 billion loan and bond offering for telecom provider Brightspeed, after struggling to attract demand from investors.

Outside of buyout deals, banks sweetened pricing on a $2.25 billion debt offering for Latam Airlines Group as they seek to cross the finish line on the company’s bankruptcy exit financing, according to people familiar. Pricing on the loan is being discussed at an all-in yield of around 15%, according to the people.

When banks committed to help financing buyouts earlier this year, high-yield debt was still relatively easy to sell. In the last six months, investors have grown more hesitant to buy, but Wall Street firms had hoped that buyers would re-emerge after the sale of debt for the buyout of Citrix Systems, an $8.6 billion offering in September.

Their hopes proved unfounded. Lenders including Bank of America, Credit Suisse Group and Goldman Sachs Group sold Citrix bonds and loans at a steep discount, realizing about $600 million of losses in the process. And they’re still sitting on $6.5 billion of debt tied to the deal.

Representatives for Barclays and Nielsen declined to comment on the Nielsen deal, while Citigroup, Tenneco and Apollo declined to comment on Tenneco. A spokesperson for Bank of America declined to comment on both transactions. Brookfield and Elliott didn’t immediately respond to requests for comment. A spokesperson for Morgan Stanley declined to comment.

For these buyouts, demand for debt could pick up in the future, and even if banks have to fund the LBOs, they can always sell bonds and loans tied to the deals later.

But now, selling buyout debt is hard in general. Globally, leveraged finance debt sales have plunged to around $315 billion this year from 2021’s $1.6 trillion, which was a record, according to Moody’s Investors Service.

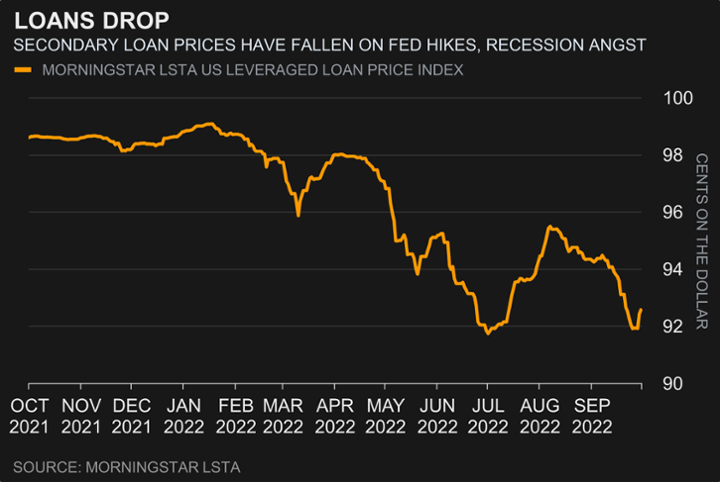

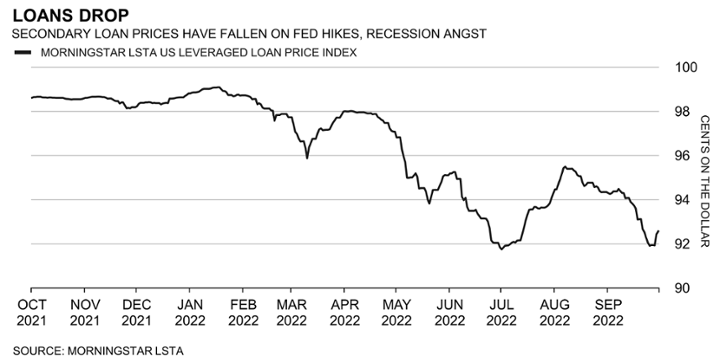

Amid this increase in perceived risk, average leveraged loan prices dipped below 92 cents on the dollar late on Sept. 30, staying there for much of this week, according to the main US leveraged loan index. In mid-September, they were around 94.5 cents, and at the start of the year, they were around 99 cents.

Credit default swap prices on Credit Suisse Group surged on Sept. 30 and Oct. 3, reaching record levels, with one-year protection jumping to more than 500 basis points. The jumps came after a memo from the bank's chief executive officer spurred concern about the firm. CEO Ulrich Koerner’s statement stressed the bank’s liquidity and capital strength, worrying investors and some Twitter pundits. Prominent figures took to Twitter over the weekend to dismiss some of the rumors circulating on social media prompted by the widened CDS spread as “scaremongering.” Saba Capital Management’s Boaz Weinstein tweeted “take a deep breath” and compared the situation to when Morgan Stanley’s CDS was twice as wide in 2011 and 2012.

Apollo Global Management acquired a minority stake in Diameter Capital Partners as the $11 billion hedge fund and CLO manager makes a foray into the private debt market. Apollo bought a 4.99% passive equity interest in the firm to back Diameter’s launch of a new direct-lending business and an expansion in Europe, according to a letter to Diameter investors. The transaction includes a commitment from Apollo to provide seed capital for Diameter’s direct-lending effort. The amount of the transaction wasn’t disclosed. Scott Goodwin and Jonathan Lewinsohn, who founded New York-based Diameter in 2017, said their fresh start during a perilous time will work in their favor.

Talks between Elon Musk and Twitter to reach a resolution of the $44 billion takeover are stuck in part over Musk’s statement that his offer is now contingent on receiving $13 billion in debt financing, according to people familiar. The billionaire’s lawyers said in an Oct. 3 SEC letter that Musk was willing to do the $54.20-per-share deal on its original terms “pending receipt of the proceeds of the debt financing.” The original deal didn’t contain such a contingency. Seven banks, led by Morgan Stanley, fully underwrote the debt portion of the financing, according to an April filing. They have always been on the hook for providing the funding if anything went wrong.

Investment firms that had expressed an interest in helping Musk finance his acquisition of Twitter abandoned the talks several months ago, around the time that the mercurial billionaire backtracked from the deal, according to people familiar. Firms including Apollo Global Management and Sixth Street Partners had been in discussions to contribute billions of dollars via a preferred equity stake -- before Musk declared the deal dead, said the people, who asked not to be identified because they weren’t authorized to speak publicly.

Juul Labs is beginning talks regarding funding for a potential Chapter 11 bankruptcy, according to people familiar. The e-cigarette manufacturer has engaged in informal talks regarding so-called debtor-in-possession financing, said the people, asking not to be named discussing private information. Formal discussions with potential lenders are expected to progress in the coming days, one of them said. In other distressed news:

The pile of troubled debt outstanding rose by about $10 billion last week, reversing a contraction from the previous week, according to data compiled by Bloomberg. The heap of dollar-denominated corporate bonds and loans in the Americas trading at distressed levels swelled to $196.7 billion on Friday, about a 5.4% increase from $186.5 billion a week earlier, according to data compiled by Bloomberg.

A Chinese developer among a rapidly dwindling group still able to access financing has found that’s no panacea amid a broader property debt crisis that policy makers are increasingly trying to defuse. CIFI Holdings Group, China’s 15th-largest developer by contracted sales this year, is among a select group of real estate firms that recently received state guarantees on local debt sales. Just weeks after that, though, its problems are rapidly multiplying, underscoring the limits to official steps to support the real estate industry.

A Chinese developer among a rapidly dwindling group still able to access financing has found that’s no panacea amid a broader property debt crisis that policy makers are increasingly trying to defuse. CIFI Holdings Group, China’s 15th-largest developer by contracted sales this year, is among a select group of real estate firms that recently received state guarantees on local debt sales. Just weeks after that, though, its problems are rapidly multiplying, underscoring the limits to official steps to support the real estate industry.

A fight over advisory fees is brewing between lenders to ailing British health-goods retailer Holland & Barrett and its Russia-linked owner LetterOne Holdings in a foretaste of the squabbles likely to come if restructurings rise amid an anticipated economic downturn. The two sides are at odds over a bill stretching to several million pounds for work done by Perella Weinberg Partners on behalf of creditors including Sona Asset Management and Credit Suisse Asset Management, according to people familiar. Lenders owed £900 million ($1 billion) joined forces to hire Perella for advice on recouping their investment after the ailing retailer’s debt fell to deeply distressed levels. They had expected LetterOne to pick up the tab, but the Holland & Barrett owner felt the work wasn’t needed and has declined to do so, said the people. Typically, companies pay creditors’ advisory fees if a formal mandate for a restructuring has been approved. LetterOne, which helps oversee more than $26.8 billion in assets around the world according to its website, didn’t engage with either the lender group or Perella, said the people.

Governments and companies around the world are facing unprecedented costs to refinance bonds, a burden that’s set to deepen fissures in debt markets and expose more vulnerabilities among weaker borrowers. A corporate treasurer or finance minister looking to issue new notes now would likely have to pay interest that’s about 156 basis points higher on average than the coupons on existing securities, after that gap surged to a record in recent days. That all adds up to about $1.01 trillion in additional costs if all those securities were refinanced, according to calculations using a Bloomberg index tracking some $65 trillion of government and corporate debt across currencies.

Investment manager Hamilton Lane is planning to use blockchain technology to make its private markets offerings more accessible to individual investors. The firm will be among the first in the $1.2 trillion private-credit market to make its funds available through tokenization -- a method of purchasing securities in the form of digital tokens using blockchain, that operates similarly to shares. Hamilton is partnering with Securitize, a digital assets securities firm, which will oversee the process.

Elon Musk’s shock proposal to proceed with his acquisition of Twitter for the original offer price means it’s now time for a group of banks led by Morgan Stanley to step up and provide financing. They committed back in April, with the intention to sell most of that to institutional investors.

Elsewhere in the US junk bond market, Canadian energy infrastructure provider Enerflex was the sole deal in market this week with $625 million of 5-year first-lien senior secured notes to help fund the acquisition of Exterran. The debt sale comes amid rising costs and renewed concerns about slowing growth, though the issuer was able to lower the yield it will offer investors from initial price discussions.

The US leveraged loan market saw one deal launch this week for Entain, a sports betting firm that came to market with a $750 million term loan to support the acquisition of SuperSport. Elsewhere, the market has been essentially closed for mega LBO deals, as secondary prices have fallen back recently and wrapped around 92 cents on the dollar and loan fund flows are expected to be negative this week.

Meanwhile, banks this week were busy sweetening pricing on a $2.25 billion debt offering for Latam Airlines Group as they seek to cross the finish line on the company’s bankruptcy exit financing. Pricing on the loan is being discussed at an all-in yield of around 15%.

US investment-grade borrowers gained some momentum this week after less than $2 billion was sold the week before. Five companies issued $5.4 billion through Oct. 5, shrugging off rising costs and recent volatility, against expectations for $75 billion for the month.

John Deere Capital and agricultural products company Cargill were among issuers to tap the market. In an encouraging development for companies, the A rated borrowers paid about 4 basis points in concessions on average on Oct. 5. That translated to about a third of the 12 basis points high-grade borrowers have offered investors to sell debt this year.

Issuance in Europe’s primary market has been choppy this week, with volatility whipsawing sentiment and limiting openings for business. Yet after a quiet start to the week, sales had reached almost 30 billion euros ($29.5 billion) by the end of Oct. 6, with the prior day seeing particularly high volumes. The ongoing economic and political uncertainty is likely to mean that steady deal flow may remain elusive in the near future.

In Asia, the Philippines sold a $2 billion three-part dollar bond, one of the few US-currency deals in Asia in recent weeks. Total demand for the offering reached $9.6 billion.

The country, along with Korea’s Hanwha Solutions, were the only issuers of dollar notes in Asia ex-Japan with a minimum $100 million size, according to Bloomberg-compiled data.

— With assistance from Olivia Raimonde, Gowri Gurumurthy, Jeannine Amodeo, Colin Keatinge, Ameya Karve and Chris DeReza

Turning Private Credit Into Equity

Mark Hootnick Tero Jänne

When credit markets get much worse, many private lenders that are tied to leveraged buyout firms could look to turn their loans into equity, said Mark Hootnick and Tero Jänne, who lead Solomon Partners’ capital transformation and debt advisory business.

They spoke to Bloomberg’s Erin Hudson in a series of interviews ended Oct. 4. Comments have been edited and condensed.

Inflation and rates are rising. Are companies feeling the pain?TJ: In the summer most companies said, “Revenue has been great, we just had a cost issue.” And as they start to go into the fall, they’re saying “well now the cost issues are even bigger, we need some third-party operational support to figure out how to cost structure this.” But now revenue is starting to come down too, especially in anything consumer discretionary. A lot of those corporates haven’t yet had to go and talk to their lenders. That’s the subsequent step that I think will start to come into play.

Anything new in recent months?

TJ: We’re hearing pretty broadly, across the parties who are involved in providing crisis management or chief restructuring officer activities, that they are getting a lot more inbound inquiries. The inbounds are both from the corporates themselves and their owners and as well as lenders who are also insisting that some of these companies, in addition to providing incremental relief on amendments or waivers, bring in expertise to try to take another look at cash flows and cost structures. And it’s even part of M&A processes. A lot of times they’re taking on initiatives that perhaps traditional management teams aren’t willing to execute – it’s very geared toward cost-cutting issues.

MH: A related point on that – and you’ve seen it in some of the bigger retail names – is the termination of the chief executive officer that is viewed as having made bad decisions or incapable of guiding the future. So the change in the C-suites of these companies as they’re going through trouble is a harbinger.

Are private credit firms stepping in to provide additional liquidity?

MH: Private credit right now is plentiful. There are people that are in the business that have never done it before and once the market cracks and their loans end up in trouble, we don’t yet know what their disposition is going to be on how to restructure that debt. A lot of the private credit funds are related to private equity shops and there could be “Hey, we own this. Let’s convert to equity. Make it part of our private equity portfolio.” There are lots of complications in your LP relationships and how you do that, but that has not really been tested yet. I think it has the potential to be a very different world.

Debt sales have struggled recently, including Apollo’s Brightspeed LBO and financing related to Latam Airlines exiting bankruptcy. What does that mean to you?

MH: The volatility is scaring people. The last thing somebody wants to do is invest and have rates continue to widen and be sitting on a loss, so I think people are taking a pause. We've had discussions about how lenders are just building cash and sitting on the sidelines. Once there’s stability and the rhetoric around the Fed lightens up, people will be more comfortable. It doesn’t mean they’ll reprice risk and everything will be cheap again, but I think you’ll see more ability to close deals.

Coercion in Europe

By Claire Ruckin

Keter Group, a maker of plastic furniture and garden sheds, is planning to pressure lenders to either give it another two years to pay back part of a loan, or find themselves stripped of key protections.

The plan is part of a broader series of transactions by Keter to deal with a €1.2 billion ($1.18 billion) loan maturing in October 2023, at a time when borrowing has become prohibitively expensive for many junk-rated companies, according to people with knowledge of the transaction.

Keter, owned by private equity firm BC Partners, is looking to press investors to go along with the transactions by changing the terms of its existing obligation: if lenders holding 80% of the loan consent to the new deal, then the current debt will be stripped of collateral, covenants and other protections for money managers, the people said.

A spokesperson for BC Partners declined to comment. Keter didn’t immediately respond to a request for comment.

Investors can resist the company’s efforts and demand to be paid back next year, but they could end up with a much riskier loan in the process. That kind of coercion is relatively unusual in Europe, but may grow more common as credit markets remain strained, making refinancing debt difficult. The average yield on a high-yield bond in Europe is close to 9%, according to Bloomberg index data, compared with just over 3% at the end of 2021.

Leveraged buyout firms that have been operating for years in a world where borrowing was cheap and easy. Now central banks globally are tightening rates to tame inflation, and getting loans is more expensive and difficult. Companies that were bought out in LBOs are getting more creative to finance maturing debt.

Keter is also planning to refinance around a third of its loan, through borrowing another €200 million of second-lien debt, and taking on additional first-lien loans as well, the people said, asking not to be quoted discussing private transactions. It’s also raised €50 million of equity to pay down some of the loan. Investors will be paid back at par on these holdings.

If investors go along with Keter’s extension, they will also receive another 1 percentage point margin, or extra interest above the benchmark rate from the loan, the people said.

All lenders have been given the opportunity to be part of the transaction, the people said. That makes this deal different from, for example, J. Crew Group’s financing in 2016, when its private equity owners stripped valuable collateral away from existing lenders in order to raise new cash, people with knowledge of the Keter loan said.

Keter is working with JPMorgan Chase to find a solution by the end of October, when the loans become current. Borrowers typically refinance 12 to 18 months before maturity. If a loan is less than a year from maturity, a company faces the risk of a credit rating downgrade that could force investors to sell its loans and securities.

A spokesperson for JPMorgan declined to comment for this story.

Under the proposed structure, the first-lien debt-to-equity ratio, a measure of how indebted a company is, will fall to around 3.9x from 4.9x, one of the people said. Keter has earnings before interest, tax, depreciation and amortization of about €223.8 million for the twelve months ended in August, the person said.

If Keter doesn’t get 80% of lenders to consent to the deal, there are other options available to the borrower, including a court-approved restructuring known in the UK as a “scheme of arrangement,” which can force all lenders to be a part of a new deal once 75% of lenders are secured, the people said.

The company postponed a loan deal in January because BC Partners thought the price for the new financing was too high. Since then, funding conditions and the macroeconomic climate have only grown worse.

Vanguard Group expects the US corporate-bond market to come under increased pressure this year as rising interest rates rattle investors and threaten businesses’ profits. Arvind Narayanan, a senior portfolio manager and co-head of investment-grade credit at Vanguard, is finding the best investment opportunities in intermediate-maturity high-grade debt, thanks to the dramatic movements in the Treasury curve that have created “near unprecedented cheapness” in those securities.

Bond giant Pacific Investment Management Co. thinks it’s now time to start buying debt. The fixed-income specialist, whose managers oversee around $1.8 trillion in assets worldwide, expects high-quality bonds to start delivering returns much more consistent with long-term averages. In contrast, it sees downside risk for global equity markets. “The return potential in bond markets appears compelling given higher yields across maturities,” Pimco’s Tiffany Wilding and Andrew Balls said in a note to clients. “We believe the case is now stronger for investing in bonds.”

Investors who found something of a haven in energy bonds during an abysmal year for credit are having to decide whether to double down or seek shelter elsewhere. The energy sector has dropped about 7.7% this year on a total return basis, but that counts as outperformance when compared with the more than 13% loss for the average high-yield credit. With junk debt generally being avoided and concern growing that a recession looms, investors are assessing whether oil credits remain a refuge.

The rising rates and high inflation that are walloping junk bond markets now will probably help private credit funds get even bigger and more powerful for the next few years, according to Preqin, a trend that can pressure Wall Street profits. The funds’ assets under management could grow at around 10.8% annually, to around $2.25 trillion by 2027, the research and data firm forecasts, as investors pour into an asset class that offers higher yields as rates rise.

The pain is just beginning for investors in US credit markets after Federal Reserve tightening and recession angst sent investment-grade bonds, high-yield debt and leveraged loans spiraling in September. While spreads are likely nearing a peak for higher-rated US corporate bonds, there’s still plenty of room for lower-rated debt spreads to widen, according to Bloomberg Intelligence’s Noel Hebert. After pressure from this week’s reading of US employment data abates, the director of credit research expects relief to seep into the investment-grade portion of the market.

A record proportion of investors expect wider credit spreads in the next three months, and their biggest concern is now the possibility of a recession, according to a September investor survey from Bank of America. “By sizable margins investors now expect wider spreads near term, tighter spreads in 12 months and only moderate credit losses,” BofA strategists led by Yuri Seliger wrote on Friday. “Incredibly, more investors now expect wider spreads in the near term than in the middle of the Global Financial Crisis in 2008.”

One of Canada’s largest pension funds is boosting its exposure to bonds, citing attractive yields after the worst selloff in a generation. The Ontario Teachers’ Pension Plan is increasing its holdings of inflation-protected debt, along with some investment-grade and junk notes, said Jo Taylor, president and chief executive officer of the fund that manages C$243 billion ($177 billion). That comes after it slashed weightings of bonds last year in favor of infrastructure and property investments to hedge against inflation.

Ethical-focused debt sales are set to pick up after the US made its biggest financial commitment in history to fight climate change, according to Fitch Group’s sustainability arm. Nneka Chike-Obi, head of APAC ESG research for Sustainable Fitch, is expecting more debt issuers to take advantage of the tax credits and other financial incentives for clean energy contained in the Inflation Reduction Act, which was signed into law in August by President Joe Biden.

Morgan Stanley has hired high-yield bond trader Jack Cook from Credit Suisse Group, according to people familiar. Cook started in his new role this week and will continue to be based in New York, one of the people said. He had been at the Swiss bank for 11 years, according to financial industry records

Oak Hill Advisors has hired Daniel Lee as a managing director in its private lending group, according to people familiar with the matter. Lee started this week in New York, according to the people, who aren’t authorized to talk about it and asked not to be identified. He will focus on GP solutions financing, reporting to Eric Muller, co-head of private credit, and Fritz Thomas, head of client coverage, the people said.

Alternative credit shop CIFC Asset Management has tapped Carlyle Global Credit’s former head of investor relations to help lead its business development efforts, according to a statement seen by Bloomberg. T. Michael Johnson moved to the business in late September, where he is working as a managing director and a global co-head of business development to lead capital formation efforts. Johnson is based in New York and will work alongside co-heads James Boothby and Joshua Hughes. The firm recently added a new chief of compliance officer and associate general counsel, Lily Wicker, and promoted Asha Richards, who had been the firm’s deputy general counsel since 2015.

Pacific Investment Management Co. is bolstering the teams that run the Total Return Fund and several other funds as Scott Mather, one of the firm’s longest-tenured executives, takes a personal leave of absence. Dan Ivascyn, the head of the flagship Pimco Income Fund, will join the management team for the Total Return Fund, as will Qi Wang, according to a regulatory filing. Other top executives, such as Mike Cudzil, Jerome Schneider, Daniel Hyman and Marc Seidner, will join the management teams of additional vehicles that Mather helped run, including the Low Duration and Moderate Duration funds and several related ESG funds. Mather and Mark Kiesel took over Total Return in September 2014 after Pimco co-founder and CIO Bill Gross shocked Wall Street by leaving the firm.

Nomura Holdings is hiring senior bankers to expand its sustainability-focused merger advisory team, betting that corporate clients will accelerate efforts to cut carbon emissions, an executive said. The Nomura Greentech group has hired five managing directors in the US over the past six months, said Jeffrey McDermott, global investment banking co-head, during the firm’s Sustainability Day forum on Oct. 6.

Law firm Clifford Chance has hired Darren Littlejohn from Fried Frank Harris Shriver & Jacobson as a partner in its US structured finance team, according to an Oct. 3 statement. Littlejohn joined the law firm as a derivatives and structured finance partner, having officially started at the company on Oct. 1, according to a company spokesperson. He covers area including credit derivatives.

Linklaters has hired Richard Woodworth as a partner based in Hong Kong for its Asia restructuring and insolvency team. Woodworth started his position this week and reports to Asia regional managing partner William Liu, he said in an interview. Woodworth joins the law firm from Allen & Overy, where Woodworth founded the firm’s Asia Pacific restructuring practice and co-headed it.

Jyske Bank has hired Klaus Grav Christensen as a vice president for the fixed income sales team, according to an update on LinkedIn. Grav Christensen previously worked as a senior dealer at Spar Nord Bank and has also been at Sydbank.

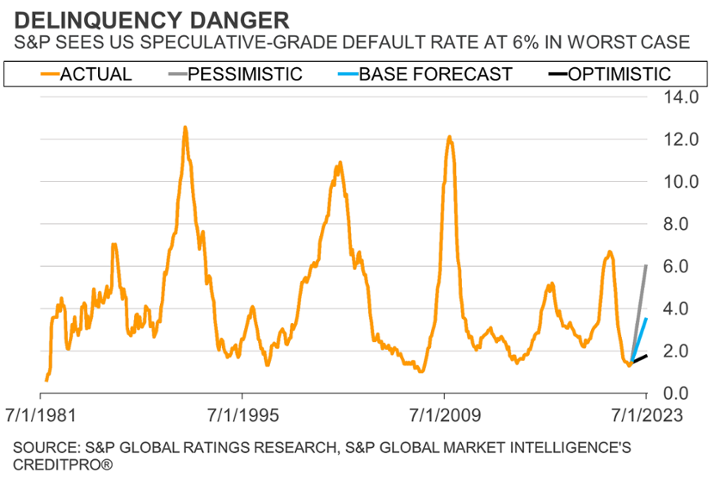

Bracing for Defaults to Spike

By Jack Pitcher

The outlook for corporate defaults is worsening quickly as cash cushions built during the pandemic erode and borrowing conditions tighten.

Analysts at Moody’s Investors Service and Citigroup both increased their default forecasts this week, a sign that the Federal Reserve’s policy of higher rates to arrest inflation may soon hurt companies with weaker balance sheets.

“Evaporating issuance will erode liquidity cushions, igniting defaults,” Moody’s analysts wrote in a report on Oct. 3.

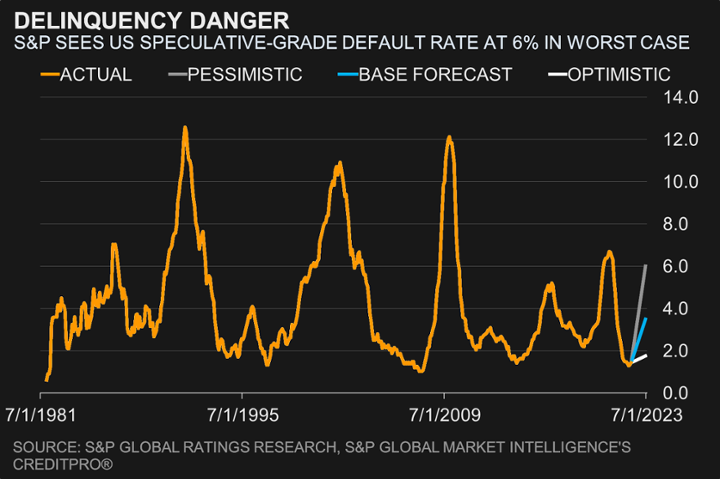

The share of companies failing to pay debt on time may jump more than threefold in the next year due to a liquidity squeeze, according to Moody’s projections.

The credit rating company’s “moderately pessimistic” forecast is for US corporate default rates to hit 7.8% by August 2023, while its baseline forecast is calling for 4.4%. That compares to a 3.7% long-term average, and a current trailing 12-month default rate of less than 2%.

Editor Responsible: Dan Wilchins dwilchins@bloomberg.net

Data: Michael Gambale mgambale2@bloomberg.net

Subscribe at BRIEF<GO>

Subscribe at BRIEF<GO>